Around May 20, import and export data for cobalt and lithium battery industry chain-related products in April were released. The data showed that in April, China's domestic spodumene imports totaled 623,000 mt, up 16.5% MoM, equivalent to 54,000 mt of LCE. Among them, lithium ore imports from Zimbabwe amounted to 106,000 mt, up 82% MoM. For lithium carbonate, China imported 28,000 mt in April, up 56% MoM and 34% YoY. Among these imports, 20,000 mt came from Chile, accounting for 71% of the total imports. In April, China exported 734 mt of lithium carbonate, up 334% MoM and 213% YoY. SMM has compiled the import and export situation of battery materials as follows:

Upstream

Lithium Concentrates

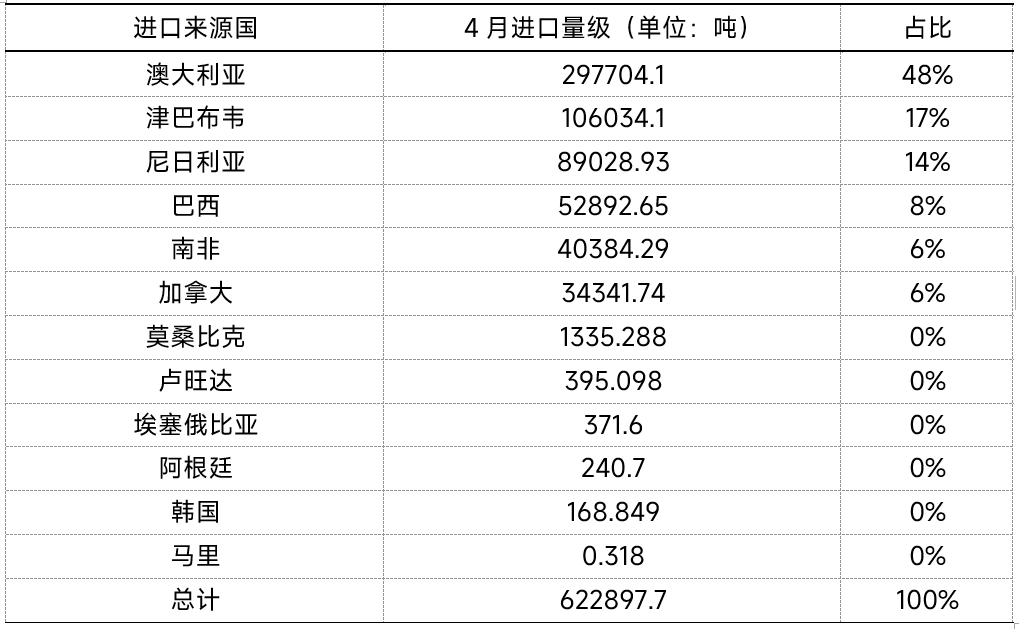

According to data from the General Administration of Customs, in April, China's domestic spodumene imports totaled 623,000 mt, up 16.5% MoM, equivalent to 54,000 mt of LCE.

Specifically, Australia, Nigeria, and Zimbabwe were the main sources of imports. Among them, lithium ore imports from Australia amounted to 298,000 mt, down 3% MoM; imports from Zimbabwe amounted to 106,000 mt, up 82% MoM; and imports from Nigeria amounted to 89,000 mt, up 4% MoM. Imports from South Africa amounted to 40,400 mt, down 22% MoM, a significant decrease.

In addition, the volume of spodumene concentrates in April was 520,000 mt, accounting for 83% of the total ore imports, mostly from countries such as Australia and Zimbabwe.

Data source: China Customs, SMM's processed data based on public information

Note: It may not be possible to fully and accurately account for the actual monthly spodumene concentrate imports from customs data, and some data are only reported in terms of the general direction of import volumes.

[SMM Analysis] In April, China's domestic spodumene imports totaled 623,000 mt, up 16.5% MoM

Returning to the current lithium ore market, on the spodumene side, according to SMM, on the supply side, although overseas mines have a certain willingness to refuse to budge on prices, due to their shipping pressure, their quotes have been adjusted downward. On the demand side, as the current lithium chemical prices are at a relatively low level, the psychological price level of buyers continues to decline, and their purchase willingness for lithium ore priced at CIF US$650/mt or above is not strong. When the current spot and futures prices of lithium carbonate are falling, demand continues to push down prices during negotiations, and the willingness to close deals is relatively moderate.

This week's lithium ore import customs data showed that in April, China's domestic spodumene imports exceeded 600,000 mt, with a significant MoM increase, equivalent to over 50,000 mt of LCE. Coupled with the high inventory levels at ports in recent months, traders and mine operators are under certain pressure to sell, enhancing buyers' bargaining power. With lithium carbonate prices remaining low, there is an expectation of weakness in lithium ore prices.

As of May 23, the spot quotation index for spodumene concentrates (CIF China) fell to $690/mt, down $127/mt from $817/mt on April 1, representing a 15.54% decline.

》Click to view SMM's spot quotations for new energy products

Lithium Carbonate

According to customs data, China imported 28,000 mt of lithium carbonate in April, up 56% MoM and 34% YoY. Of this, 20,000 mt was imported from Chile, accounting for 71% of the total imports, and 6,850 mt was imported from Argentina, accounting for 25% of the total imports. From January to April, China's cumulative imports of lithium carbonate reached 79,000 mt, up 27% YoY. In April, China exported 734 mt of lithium carbonate, up 334% MoM and 213% YoY.

Reviewing the current lithium carbonate prices, according to SMM's spot quotations, as of May 23, the spot quotation for battery-grade lithium carbonate temporarily held steady at 61,600-64,500 yuan/mt, with an average price of 63,050 yuan/mt, down 11,050 yuan/mt from 74,100 yuan/mt in early April, representing a 14.91% decline.

》Click to view SMM's spot quotations for new energy products

Reviewing the lithium carbonate market in April, downstream power demand performed well, but was constrained by the impact of the cancellation of mandatory ESS allocation in China and US tariff policies, limiting the overall increase in demand. Additionally, with the increase in the proportion of customer-supplied raw materials at downstream material plants, their willingness to purchase spot orders weakened. Supply side, the continuous decline in prices led some non-integrated lithium chemical plants to reduce or halt production, but the impact was limited in scale. Lithium carbonate remained in a state of surplus that month, with the surplus scale narrowing somewhat.

Looking at the current situation, according to SMM, from the supply side, some enterprises have shown signs of maintenance and production cuts, with weekly output scales weakening. However, under the hedging opportunities presented by the slight rebound in the futures market, some non-integrated lithium chemical plants are expected to resume production or show signs of increasing output. Overall, while the reduction in output due to maintenance has exerted some pressure on the total output of lithium carbonate, overall supply is expected to remain at a relatively high level.

Although downstream demand also saw some increase in May, due to the currently large proportion of customer-supplied and long-term contracted materials, and with the continuous decline in lithium carbonate prices, downstream material plants are generally adopting a cautious wait-and-see attitude, making it difficult for spot order transactions to support market confidence.

From the perspective of the raw material ore side, prices have also continued to decline, and no mines have announced production cuts or halts. With the continuous weakening of cost support, lithium carbonate prices lack upward momentum. Against the backdrop of an unchanged surplus in supply and demand, SMM expects the lithium carbonate market to remain under pressure in the short term.

Lithium hydroxide

According to customs data, China's lithium hydroxide exports reached 4,222 mt in April, remaining basically flat MoM and decreasing by 61% YoY.

Of this, exports to South Korea amounted to 2,047 mt, accounting for 48% of China's total exports, decreasing by 6% MoM and 72% YoY. Exports to Japan reached 1,756 mt, accounting for 42% of China's total exports, decreasing by 7% MoM and 40% YoY. The average export price of lithium hydroxide from China in April was $14,297/mt, up 8% MoM. Since the beginning of 2025, weak overseas downstream demand, coupled with the partial transfer of overseas lithium hydroxide orders for domestic shipments, has led to a sustained low level of exports. Additionally, China's lithium hydroxide imports in the same month amounted to 1,276 mt, decreasing by 35% MoM. Of this, imports from Australia and Argentina amounted to 1,094 mt, accounting for 86%, primarily due to the sales of inventory and output from Chinese-funded smelters in Australia and the production from salt lakes in Argentina.

Data source: General Administration of Customs, compiled by SMM

》【SMM Analysis】China's lithium hydroxide exports reached 4,222 mt in April, basically flat MoM

Battery materials

LFP

According to the latest data from the General Administration of Customs, China's LFP exports amounted to 1,151.7 mt in April 2025, decreasing by 16% MoM from March and increasing by 1,724% YoY. In terms of prices, the average export price of LFP in March 2025 was $6,206.9/mt, up $315.55/mt from the average price in March, representing a MoM increase of approximately 5.4%.

In the import data of the General Administration of Customs for April 2025, Guangxi Zhuang Autonomous Region remained the top province for LFP exports, with 968.5 mt, all exported to Vietnam. Hubei Province ranked second with 59.454 mt, and Anhui Province ranked third with 30 mt.

In terms of country-specific export data for LFP in April 2025, Vietnam remained the top export destination, with a total of 968 mt of LFP exported to Vietnam, accounting for 84% of total exports. South Korea ranked second with 7%, and Taiwan, China ranked third, with 63 mt of LFP exported to Taiwan, China, accounting for 5.5% of total exports. There were also exports to France, Italy, the US, Greece, etc.

Additionally, according to China's customs import data, China's LFP imports in April amounted to 8.6 mt, decreasing by 58% MoM, primarily imported from Indonesia, with an average import price of $5,345.6/mt.

》【SMM Analysis】China's LFP import and export situation in April

Ternary cathode

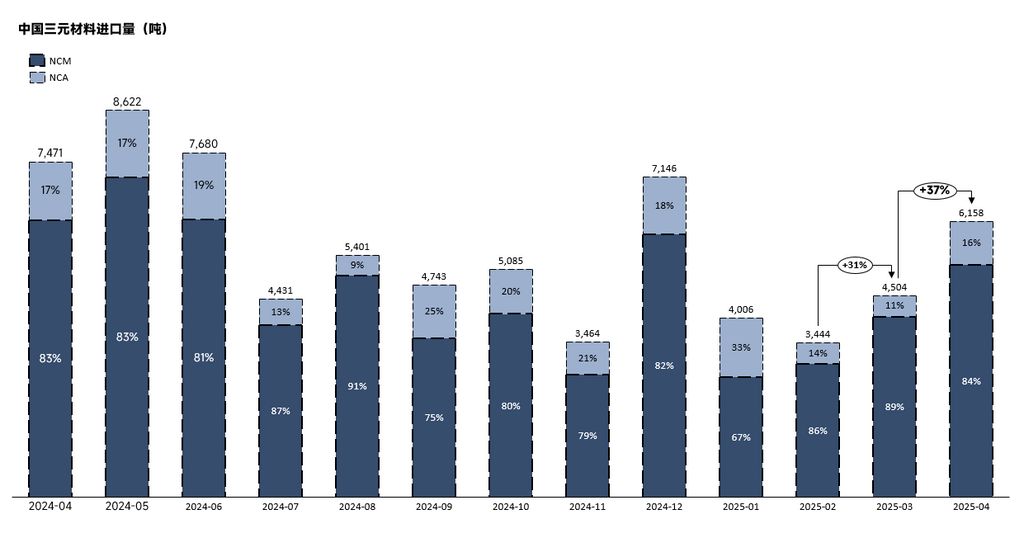

In April 2025, China's imports of ternary cathode materials (combined NCM+NCA) amounted to 6,158 mt, increasing by 36.73% MoM and decreasing by 17.58% YoY. Among them, NCM imports reached 5,170 mt, up 28.48% MoM and down 16.21% YoY. NCA imports stood at 988 mt, up 105.94% MoM and down 24.07% YoY.

In April 2025, China's exports of ternary cathode materials (combined NCM and NCA) amounted to 9,356 mt, up 13% MoM and up 30% YoY. Among them, cumulative NCM exports reached 9,058 mt, up 11.31% MoM and up 30.86% YoY. The recovery in overseas demand was mainly reflected in South Korea, Japan, and Poland. Exports to South Korea in April were 4,725 mt, up 104 mt MoM. Exports to Japan were 1,016 mt, up 349 mt MoM. Exports to Poland were 1,539 mt, up 349 mt MoM. NCA exports were 298 mt, up 90.29% MoM and down 0.71% YoY.

Ternary cathode precursor

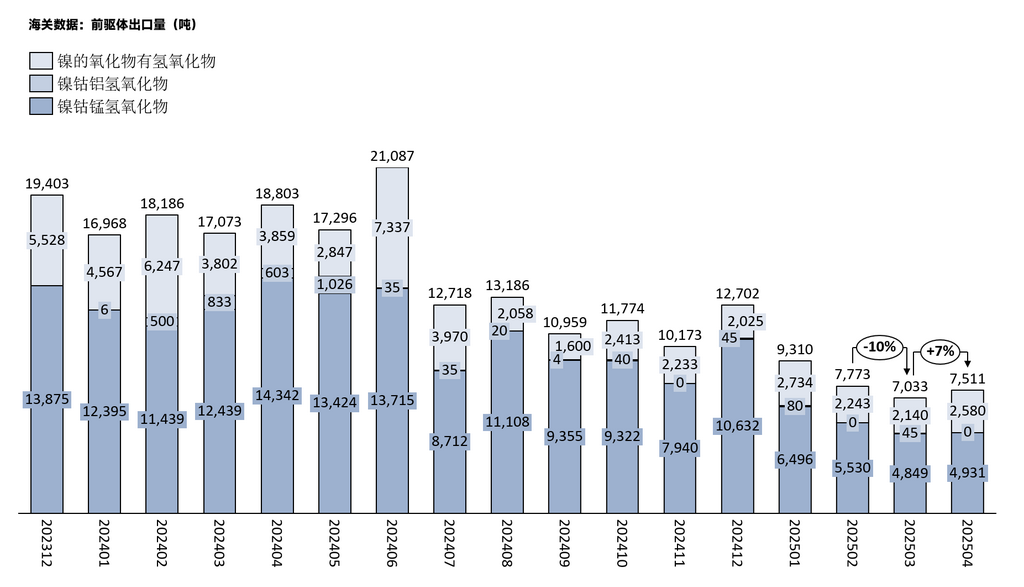

In April 2025, China's exports of ternary cathode precursors reached 7,511 mt, up 7% MoM and down 60% YoY.

From May 2024 to April 2025, China's cumulative exports of ternary cathode precursors (including NCM, NCA, nickel oxides, and NC) were 141,523 mt, down 16.70% YoY.

In April, the overall export volume of ternary cathode precursors increased compared to March. Among them, the export volumes of NCM and NC rebounded, while the export volume of NCA decreased significantly. The total NC exports in April were 2,580 mt, up 20.56% MoM and down 33.13% YoY. NCA exports in April were 0 mt. In addition, the total NCM exports in April were 4,931 mt, up 1.69% MoM and down 65.62% YoY.

By country, South Korea remained China's main export destination for NC in April, though its share decreased slightly to 90%, with export volume increasing from 1,605 mt the previous month to 2,331 mt. The volume of NCM flowing to South Korea decreased from 4,546 mt the previous month to 4,426 mt.

》[SMM Analysis] Analysis of ternary cathode precursor exports in April

Artificial graphite

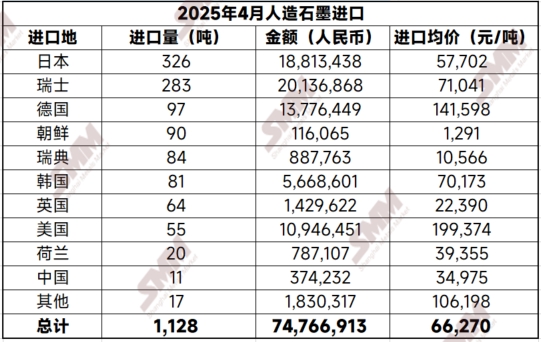

In April 2025, China's imports of artificial graphite were 1,128 mt, up 10% MoM and up 1% YoY. In terms of average import price, in April 2025, the average import price of artificial graphite in China was 66,270 yuan/mt, up 219% MoM and down 8% YoY.

Data source: SMM, China Customs

In April 2025, China's exports of artificial graphite were 58,170 mt, up 30% MoM and up 19% YoY. In terms of average export price, in March 2025, the average export price of artificial graphite in China was 9,190 yuan/mt, down 13% MoM and down 32% YoY.

In April 2025, against the backdrop of domestic coke prices not yet falling to low levels, domestic anode material enterprises showed low production enthusiasm, and domestic supply was slightly tight. As a result, the import volume of artificial graphite increased MoM. On the export side, affected by tariffs, the volume of artificial graphite exported to the US in April decreased by 29% MoM. Except for the US, the import volume of artificial graphite from China by other countries all increased to varying degrees.

》[SMM Analysis] In April, the import and export volumes of artificial graphite both increased MoM.

LiPF6

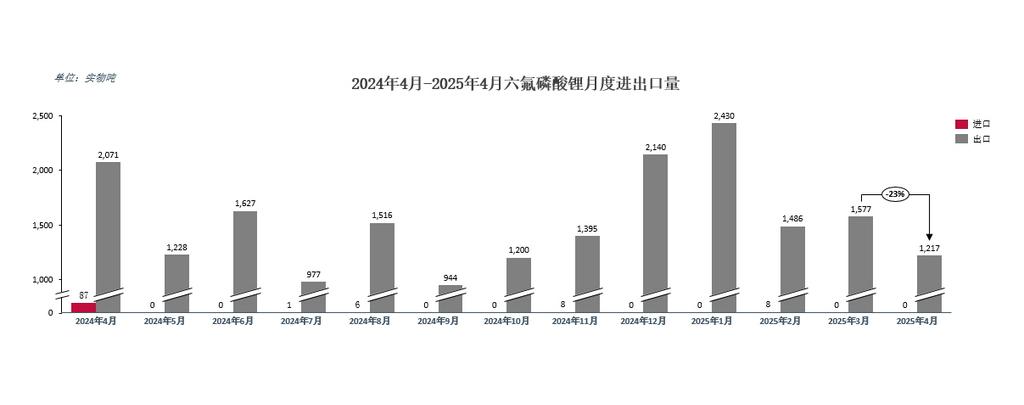

According to data from China Customs, in April 2025, China's cumulative export volume of LiPF6 was 1,217 mt, a decrease of approximately 23% MoM. Among them, China's cumulative import volume of LiPF6 was 0 mt.

On the export side, in April 2025, China's export volume of LiPF6 was 1,217 mt, a decrease of approximately 23% MoM from March and approximately 41% YoY. Specifically, 371.404 mt of LiPF6 was exported to Poland, an increase of approximately 48% MoM; 225 mt was exported to Hungary, an increase of approximately 66.7% MoM; 171.212 mt was exported to South Korea, a decrease of approximately 41% MoM; and 107.847 mt was exported to the US, a significant decrease of approximately 78.7% MoM.

Overall, there was a certain decrease in the procurement volume of raw materials for lithium batteries by foreign countries in April, and overseas demand for lithium batteries declined.

》[SMM Data] Import and Export Data of LiPF6 in April 2025

Cobalt

Cobalt hydrometallurgy intermediate products

According to customs data, in April 2025, China's import volume of cobalt hydrometallurgy intermediate products was approximately 18,600 mt (metal content), an increase of 5% MoM. In terms of average import prices, in March 2025, the average import price of cobalt hydrometallurgy intermediate products in China was $15,820/mt (metal content). By country, in March, the DRC remained the main importing country, with an import volume of approximately 18,500 mt (metal content) (calculated based on a grade of 35%), an average import price of $15,857/mt (metal content), and an import share of approximately 99%.

》[SMM Analysis] In April, the import volume of cobalt intermediate products increased slightly.

Unwrought cobalt

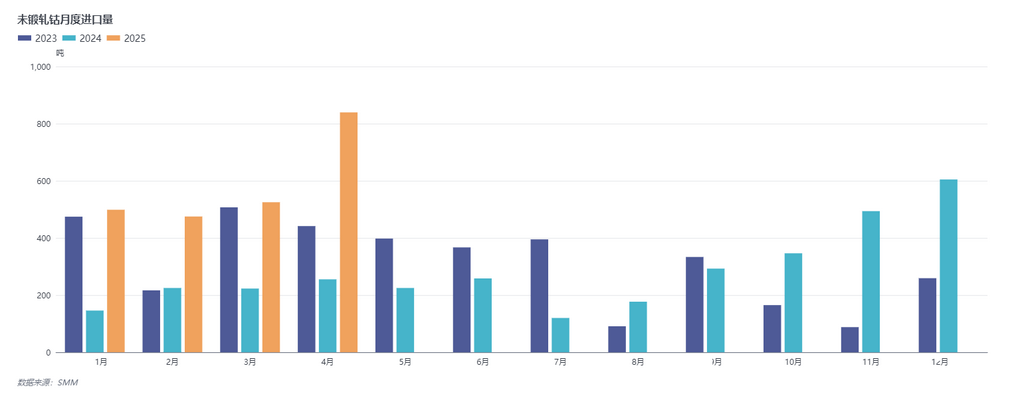

In April 2025, China's import volume of unwrought cobalt was approximately 839 mt (metal content), an increase of 60% MoM and 230% YoY. In terms of average import prices, in April 2025, the average import price of unwrought cobalt in China was $26,831/mt (metal content), an increase of 36% MoM. From January to April 2025, the cumulative import volume was 2,337 mt (metal content), a cumulative increase of 175% YoY.

On the export side, in April 2025, China's export volume of unwrought cobalt was approximately 4,086 mt (metal content), an increase of 201% MoM and 556% YoY. In terms of average export prices, the average export price of China's unwrought cobalt in March 2025 was $31,119/mt (metal content), up 28% MoM. The cumulative export volume from January to April 2025 was 7,397 mt (metal content), up 185% YoY.